- While banks are still figuring out how to underwrite electric vehicles, fintech startups have pulled far ahead and captured the EV financing market

- Of the total financing for EV two-wheelers, 63% comes from fintech startups; the remaining comes from banks, according to OTO Capital

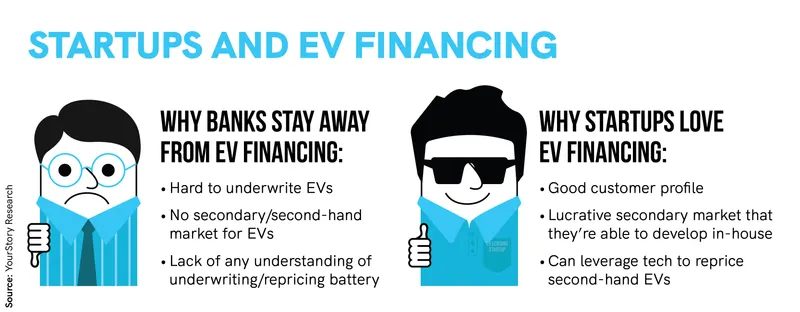

- According to experts, banks have fallen behind when it comes to EV loans because of two main reasons: lack of understanding when it comes to battery, and absence of a secondary market

- Startups like OTO Capital and RevFin, however, are developing secondary markets for EVs

Exhausted and disheartened, Arun Kumar, a software engineer at Google, found himself trapped in an endless maze of bureaucracy while desperately seeking a bank’s approval for a Rs 1 lakh loan to fulfil his dream of acquiring the coveted Ather 450X.

“Over the last five months, I’ve applied for loans at all the big banks I could think of. Each loan application cycle took a month to complete…I had to provide a carton-worth of documents. And each time, I’ve been rejected,” he says.

Despite his robust credit score, impeccable income statements, and diligent credit card repayment practices, Kumar faced crushing disappointment as not just one, but two public sector banks and two private banks turned down his loan application.

“I ran into a loan agent outside one of the banks one day, and I showed him my application and asked him why I kept getting rejected. He said, ‘It has nothing to do with you or the documents, banks just say NO to loans for electric scooters.’ That was surprising because the government has been pushing for EVs so much,” says Kumar.

Fed up of knocking on banks’ doors for almost six months, Kumar decided to look for private lenders and found a couple of them online. In less than three days—and after applying for a loan without having to leave the comfort of his home in Bengaluru—an Ather 450X was at his doorstep.

Although Kumar acknowledges that he may incur a slightly higher interest rate than if he had obtained the loan from a traditional bank, he extols the additional features provided by the startup from which he secured the loan—a guaranteed buyback in case he decides to sell his scooter, the option to upgrade to a newer model on the same EMI plan, cheaper battery when it’s time for a replacement, and discounts from insurers, among a host of other benefits.

Kumar’s experience is emblematic of a broader trend in the electric vehicle (EV) ecosystem, where more and more startups are leading the charge when it comes to financing, versus traditional banks.

Of the total financing for EV two-wheelers, 63% comes from fintech startups; the remaining comes from banks, according to OTO Capital.

Experts, including EV financing entrepreneurs, investors, and analysts, attribute the banking industry’s reluctance to venture into the EV space to a fundamental lack of understanding.

“The rapid advancements in technology, evolving regulations, and unique financing models specific to the EV industry present a considerable learning curve for traditional financial institutions. We recognise the potential of this burgeoning sector, but until we gain a comprehensive understanding of its nuances, we have to proceed cautiously,” a representative from a private bank, who Kumar had also approached, tells YourStory.

Startups show the way

According to EV financing startups, there are several overarching reasons why banks don’t view EV loans favourably, starting with underwriting practices.

Typically, in the banks’ view, an internal combustion engine (ICE) vehicle derives its value from its make, model, and especially its resale value if it has to be repossessed due to non-repayment of a loan.

Banks have been giving auto loans for several decades, and they know the value they might get out of a car if they have to sell it second-hand to recoup their money; but EVs are a different ball game, says an investor in the EV space who did not wish to be named since some banks are his firm’s limited partners.

Approximately, 40% of the total cost of an EV is its battery, which naturally degrades over time. On average, EV batteries are expected to last around three to four years, which is typically the duration of an auto loan.

If a bank has to repossess a vehicle in the third year of its running, by which time the battery has deteriorated, reselling in the secondary market may prove futile and financially unviable because potential buyers could be reluctant to invest substantial sums of money to replace the battery and make the vehicle operational.

Sure, buyers could always switch to a battery-swapping model and not own the battery at all. But not all vehicles have swappable battery packs—some come with fixed batteries.

Moreover, banks are not likely to get into the trenches to figure out this complex issue, which entails partnering with multiple vendors for the battery side of things.

“At least not this early,” the investor says.

The bigger obstacle for banks though is that secondary or re-sale markets for EVs are few and far between.

“Secondary markets are important for banks because they need to recover the value of the asset if a loan is not repaid. Very few second-hand dealers have actually been able to figure out how to re-price EVs, but startups have done a good job of it,” says Kunal Khattar, Founder of , an early cheque VC firm, and one of ’s early backers.

Even when banks do sanction e-vehicle loans, they’re more likely to do it for four-wheelers than two-wheelers, a bank representative quoted earlier in the story, says. Banks assume that people taking car loans are more likely to have stable jobs, good incomes, and decent credit history.

Two-wheeler loans are generally considered riskier because, more often than not, they’re sought by individuals with limited credit history or lower income levels.

A tech-driven process

, a startup that helps people get quick loan approvals for purchasing electric two-wheelers says its data shows that EV two-wheeler buyers default less frequently on their loans than ICE scooter owners.

People who apply for EV financing are tech savvy, educated, have good jobs, and are typically high earners, given the fact that they’re willing to spend more purchasing an electric scooter than buy the cheaper combustion-engine equivalent, says Sumit Chhazed, CEO and Co-founder of OTO, citing internal data.

“Our NPAs (non-performing assets, i.e., loans that haven’t been repaid) are very marginal because we’ve realised that EV buyers are more inclined to repay their loans consistently and diligently compared to owners of combustion-engine vehicles.”

Of course, it also helps that EV owners don’t have to spend an inordinate amount of money every week or month on petrol or diesel, which again ensures timely payments of EMIs.

According to Tracxn, there are 898 EV-focussed startups in India. Of these, only a handful do end-to-end financing of EVs. Some of these include OTO, , , Greaves Finance, , etc.

Most of the startups in the space have partnered either with banks or NBFCs to extend their loans to buyers. Others have leveraged credit lines from foreign funds who want to get into the EV space.

OTO, for example, has tied up with several NBFCs and funds such as Trillionloans Fintech, Grow Money Capital, Western Capital Advisors, and Northern Arc Capital, among others. RevFin counts Arthmate, Caspian Debt, Northern Arc, PACE Finance, and UC Inclusive Credit as its lending partners.

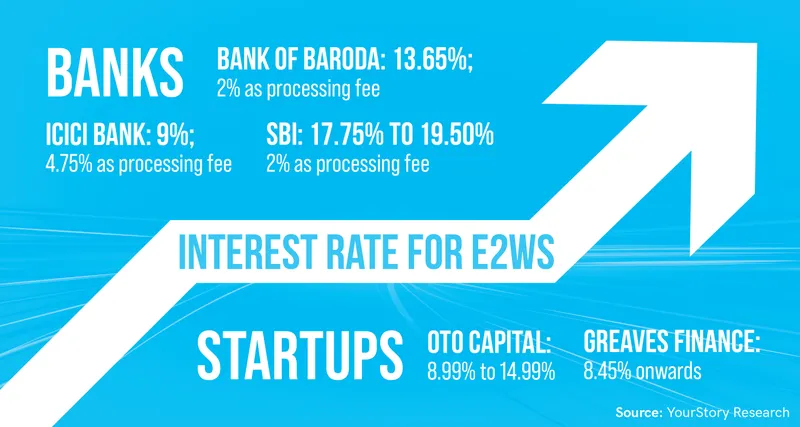

Startups typically borrow money from these NBFCs, banks, and investors at an interest rate of around 4-5%, and charge customers 12-18%.

While quantifying the exact number of EV loans sanctioned by banks compared to startups is challenging—especially since some banks have partnered with them to facilitate EV loans—startups assert they have the capacity to underwrite loans more precisely and efficiently than traditional financial institutions.

And that’s mainly because of their tech.

“EVs are basically the smartphones of automobiles,” says Sameer Aggarwal, Founder and CEO of RevFin, a fintech company that provides loans for EV fleets.

“Every second, EV sensors gather an extensive array of data points that can help piece together the complete life story of the vehicle, including information such as its usage patterns, the types of terrains it has traversed, the driving behaviour exhibited by the driver, charging and discharging cycles, and even how the battery has been treated… basically aspects like drops and voltage surges,” he explains.

Startups leverage this data intelligently and use telemetry to not only encourage good driving behaviour—which can translate into incentives for borrowers when they pay EMIs— but also, and more importantly, underwrite the vehicles when they come back to the secondary market.

“Because an EV can provide extensive insights into the battery health and remaining lifespan, we can accurately price them when they enter the second-hand market. And we’ve seen that the level of accuracy with which we’re able to put a price tag on second-hand EVs surpasses even that of combustion engine vehicles, which are typically priced based on superficial factors like scratches and general wear and tear,” OTO’s Chhazed says.

Which is why startups are winning the race when it comes to writing loans for EVs.

Why personal loans don’t make the cut

Taking a personal loan to cover the cost of a vehicle isn’t unheard of in India. Banks tend to look at personal loans as an umbrella category, and because they are so easily accessible, application is a much less arduous process.

A question that naturally arises is why buyers can’t opt for a personal loan to fund their EV purchases.

“The biggest advantage of auto loans is the tax breaks on interest that the government gives,” says OTO’s Chhazed.

Under Section 80EED of the Income Tax Act, buyers are allowed to claim tax savings of up to Rs 1.5 lakh on interest paid on a loan availed for an EV purchase. But this is only applicable to electric cars.

For electric two-wheelers, personal loans become quite costly compared to auto or bike loans, and for India, a price-sensitive market, that can make a significant difference in affordability and overall ownership experience for individuals.

Absence of government support

According to a NITI Aayog report, India’s transition to EVs needs as much as Rs 19.7 lakh crore between 2020 and 2030. That figure includes EV infrastructure, including charging and swapping stations, as well as manufacturing facilities, among others.

It also includes purchases by people who ditch combustion engine vehicles and purchase EVs.

And while EV adoption is an important target for the government, financing, unfortunately, does not yet fall under priority sector lending.

“Inclusion for retail lending to EVs has the potential to increase investor confidence by providing a market signal of ongoing government commitment to the sector,” says NITI Aayog.

“It can also ensure a swift and equitable transition by providing a mandate for financial institutions to direct credit to segments and use cases where credit deficiency persists despite compelling economics,” the NITI Aayog report that proposes the inclusion of EV financing in the Reserve Bank of India’s priority-sector lending guidelines, says.

Essentially, if the government prioritises making lending to EV buyers a mandate for banks, it can significantly enhance the adoption of EVs.

The NITI Aayog’s e-Amrit portal, which provides information about electric mobility in India, lists The State Bank of India, Axis Bank, Ujjivan Small Finance Bank, and Credit Fair as some financial institutions that offer EV loans. The average interest rate being charged by these lenders is between 12-18% for two-wheelers, which closely aligns with interest rates offered by startups.

For four-wheelers, it is 6.5-11%.

Up until now, EV adoption, especially in the two-wheeler segment, has been driven by FAME subsidies. With the industry now expecting those to reduce or be scrapped completely, the availability of cheaper, more affordable loans will emerge as the decisive factor for those considering the transition to EVs.

Amidst the unstoppable rise of electric vehicles (EVs), the main question that looms is this: Will banks, driven by the undeniable force of EVs, enter EV financing, or will they find themselves lamentably tardy, unable to seize the opportunity that awaits?