da-kuk

Thesis

With the launch of its new Artificial Intelligence Platform (AIP), Palantir (NYSE: PLTR) has rebranded itself as an AI company. With 20 years of experience in data and a long list of partners that it can offer its new product to, I personally believe that it will be a leader in the AI sector. Furthermore, Palantir is continuing to showcase its strong relationship with the U.S. government with two new contract wins over the last two months.

Additionally, I expect Palantir to beat its management’s and analysts’ revenue forecast of $532 million and will post an EPS in line with analysts’ estimates of $0.01, which is why I give Palantir a buy rating.

Q1 Financial Overview

In Q1 2023, Palantir realized $525 million in revenue, beating its own revenue estimates of $503 million – $507 millions and recording 18% YoY growth. Additionally, the company achieved positive operating income for the first time in its history and profitability for the second consecutive quarter.

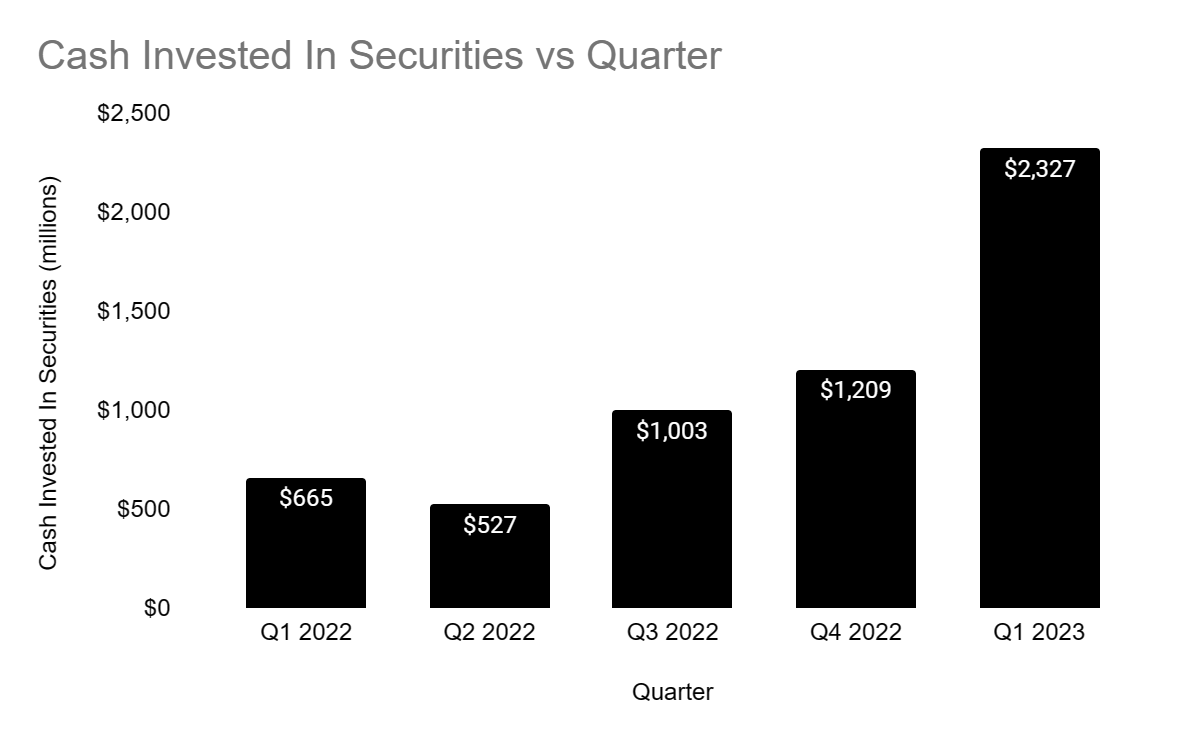

The main driver of Palantir’s profitability is interest income which has increased to $20 million from only $0.5 million in Q1 2022. The exponential growth of 4000% was due to increasing interest rates and the company investing more of its assets in interest-generating securities such as US Treasury securities.

Earnings Report

While I believe it was smart of Palantir to capitalize on the high interest rates and increase its investment in securities, I think we need to see further improvement in its operating income in the next couple of quarters, especially with the launch of AIP, which should drive revenues up.

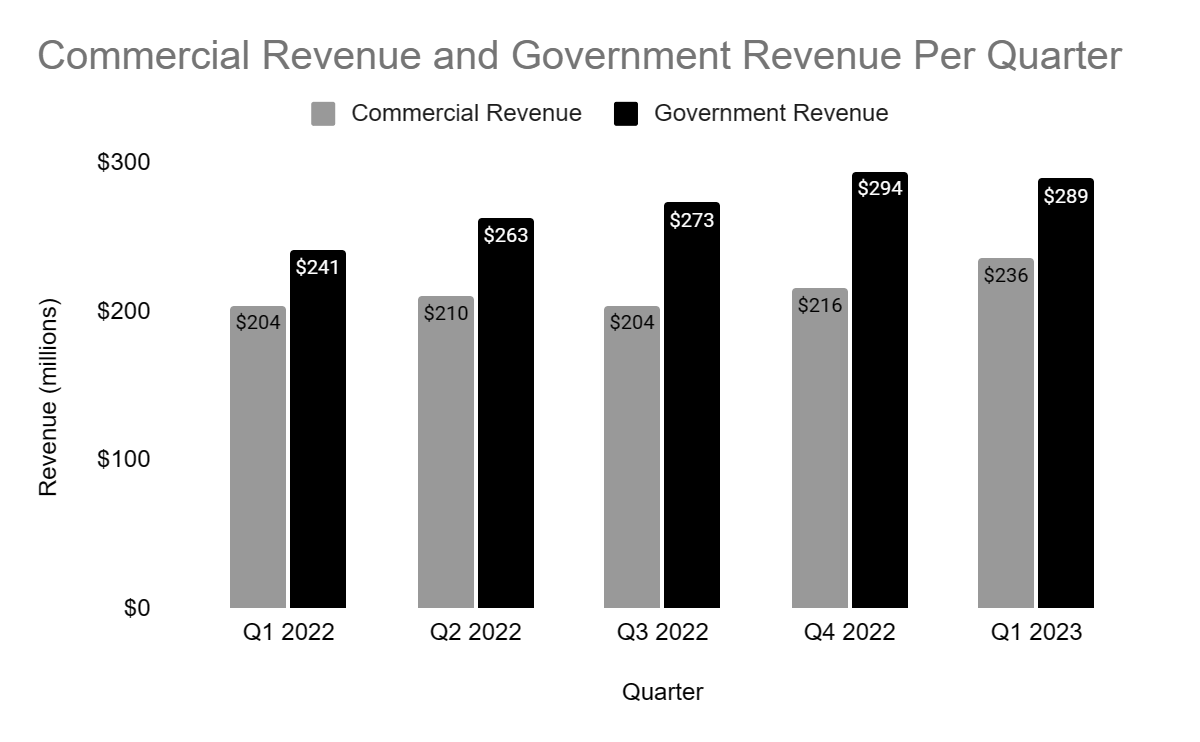

Palantir has increased both its commercial customer count to 280 customers and its government customer count to 111 customers which represents 8% and 4% growth rate respectively. Government-related revenue still makes up the majority of its revenue despite seeing a slight decline from $294 million in Q4 2022 to $289 million in Q2 2023.

Earning Report

AIP Demand

Since the launch of AIP, there have been a lot of discussions about whether its launch is enough to call Palantir an AI company and whether there’s actual demand for the product. First of all Palantir has always been an AI company, while it may have not advertised itself as such, products like Foundry and Apollo always had AI elements in them. What the company did with the launch of AIP is putting AI at the forefront and highlighting its AI capabilities making it a main part of its products and not just a complimentary element.

While CEO Alex Karp has stated multiple times that there is an unprecedented demand for AIP, many were still skeptical. What I believe people are missing is that AIP can be a standalone product or it can be integrated with the company’s existing products like Apollo and Foundry. That means that Palantir can offer AIP to its existing customers, which will drive demand initially since it has a long list of customers that is still growing QoQ.

This is exactly what Palantir did and showcased in AIPCon which I recommend watching to gain a deeper understanding of how its partners, which include big names like Cisco (NASDAQ:CSCO), Panasonic (OTC: PCRFY) and Jacobs Solutions (NYSE: J), will integrate AIP.

Another area where I think people might misunderstand AIP is the comparison with Microsoft’s (NASDAQ: MSFT) ChatGPT. While ChatGPT may be more well known to the public, it is not what Palantir’s customers are looking for in an AI tool since they’re looking for a customizable AI tool that can interact with their own data to drive solutions and insights from it. That makes Palantir special, since it can be a one stop shop for many companies since it provides both the data management tools and an AI that can interact and provide insights and solutions from this data.

That is why I believe demand will not be a problem for Palantir in the future, be it for its data tools or for the new AIP product.

Q2 Forecast

In the Q1 earnings call, management forecasted Q2 revenue to be between $528 million and $532 million. Meanwhile, analysts expect Palantir’s EPS to be around $0.01 and its revenue to be slightly higher than the management’s high-end forecast of $532 million. I believe the company will beat the revenue estimates and post an EPS in line with estimates.

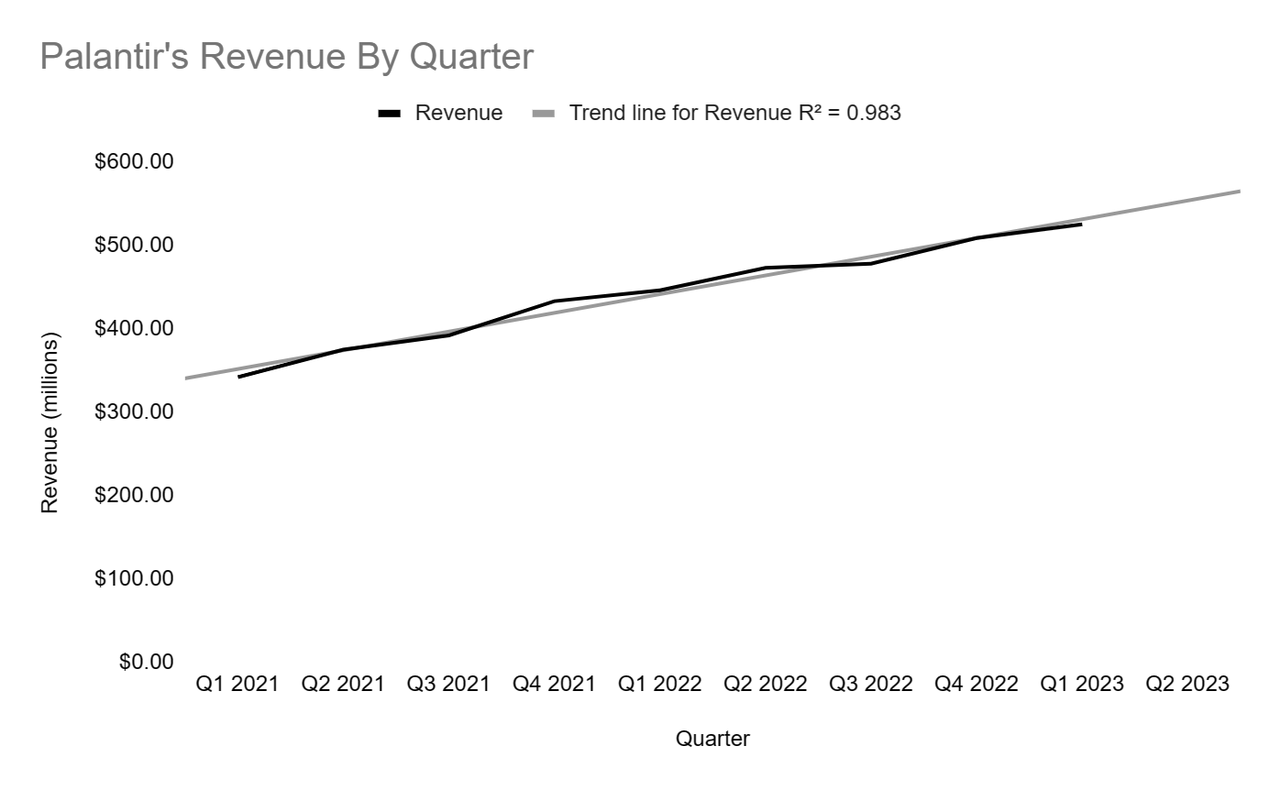

Looking at Palantir’s revenue by quarter, we can see that it is following an upward linear trend with a high correlation coefficient (R) of 0.991, which makes linear regression more than suitable for forecasting its Q2 revenues.

Earning Report

According to the chart above, Palantir’s Q2 revenue projection is $553 million, which is consistent with its YoY revenue growth over the last couple of quarters.

|

Quarter |

Revenue |

Revenue Growth |

|

Q1 2022 |

$446.00 |

30.41% |

|

Q2 2022 |

$473.00 |

26.13% |

|

Q3 2022 |

$478.00 |

21.94% |

|

Q4 2022 |

$508.60 |

17.46% |

|

Q1 2023 |

$525.20 |

17.76% |

|

Q2 2023 |

$553.53 |

17.03% |

However, revenue may differ from the forecast if Palantir experiences slower customer count growth, which I believe will not be the case due to the release of AIP as it will increase demand for the company’s products in my opinion.

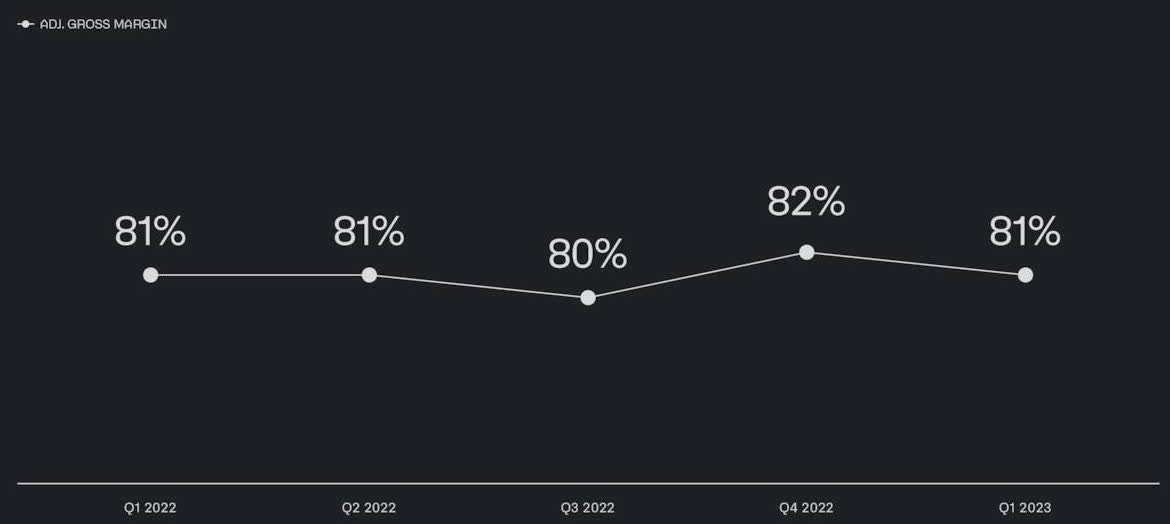

Moving to operating income, management forecasted adjusted operating income to be around $120 million. Since adjusted operating income is operating income without stock based compensation added, that means the operating income projection should be around $6 million if we assume that stock based compensation stayed the same as Q1 at around $114 million. We can also forecast Palantir’s gross margin to be 81%, as it has been consistently in the low 80’s and has averaged around 81% over the last five quarters.

Q1 2023 Presentation

Furthermore, since interest rates increased throughout Q2 and averaged around 5.17% compared to 4.75% in Q1, Palantir’s interest income projection should be around $22 million, assuming it didn’t sell any of its interest-generating securities or add new ones from Q1. All of that adds up to a net income projection of $28 million or an EPS GAAP estimate of $0.01.

|

All in millions except EPS |

|

|

Revenue |

$553 |

|

Gross Profit |

$450 |

|

Operating Expenses |

$444 |

|

Operating Income |

$6 |

|

Interest Income |

$22 |

|

Net Income |

$28 |

|

Shares Outstanding |

2,120 |

|

EPS |

$0.01 |

Technical Analysis

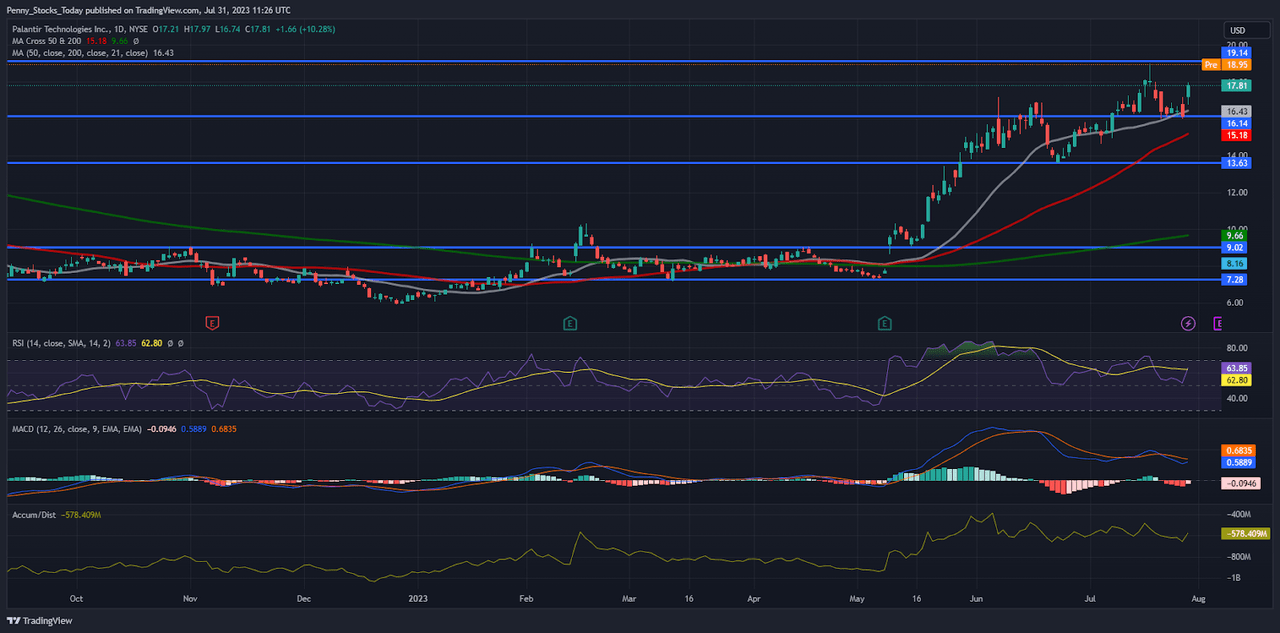

PLTR technical analysis

Looking at the daily chart, Palantir’s trend is neutral with the stock trading in a sideways channel between $16.14 and $19.14. As for the indicators, the stock is trading above the 21, 50, and 200 MAs, which is a bullish indication. Meanwhile, the RSI is neutral at 64 and the MACD is approaching a bearish crossover.

While I believe Palantir is a long term investment, buying before its Q2 earnings may prove beneficial in case it beats its revenue estimates as my projections show.

Risks

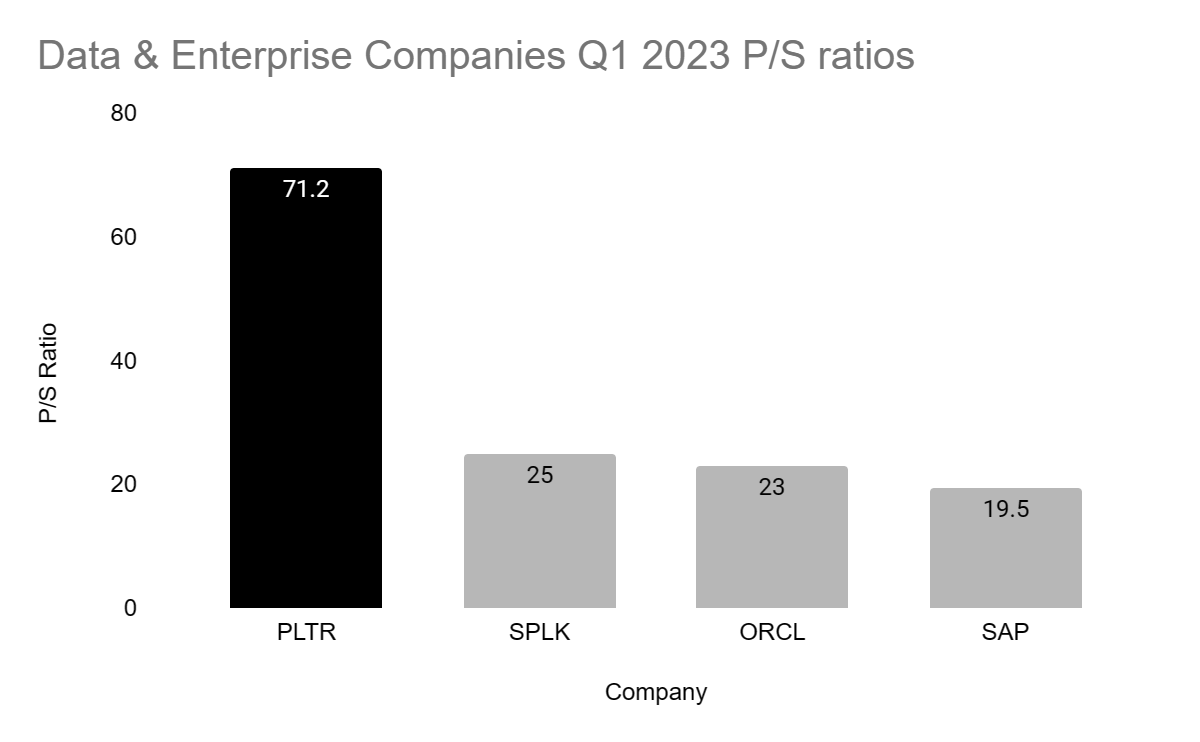

Since PLTR has increased more than 178% YTD, a lot of talks about the company being overvalued started, especially when comparing its P/S to other data centric companies like Splunk (SPLK), Oracle (ORCL) and SAP (SAP).

PLTR, SPLK, ORCL and SAP Q1 earnings

This means that in case Palantir misses on revenue and EPS forecast its share price will likely plummet since some investors still consider it overvalued at its current price per share. Another risk is the tough competition in the AI space from Microsoft and Google and in the data analytics space from Splunk and Oracle, which may limit Palantir’s growth in the commercial segment.

Conclusion

While some investors may think that Palantir is overvalued compared to other data centric and AI stocks, I believe that they’re valuing it from the wrong angle. The company should be valued based on its AI prospects as well as the value it can bring to the AI and data spaces. Adding to that is the fast rate at which it has been bringing in new customers. Furthermore, the company is a government favorite, which is why it keeps winning new government contracts. Since I’m projecting the company to beat its revenue estimates while achieving its third straight quarter of profitability, I’m giving Palantir a buy rating.